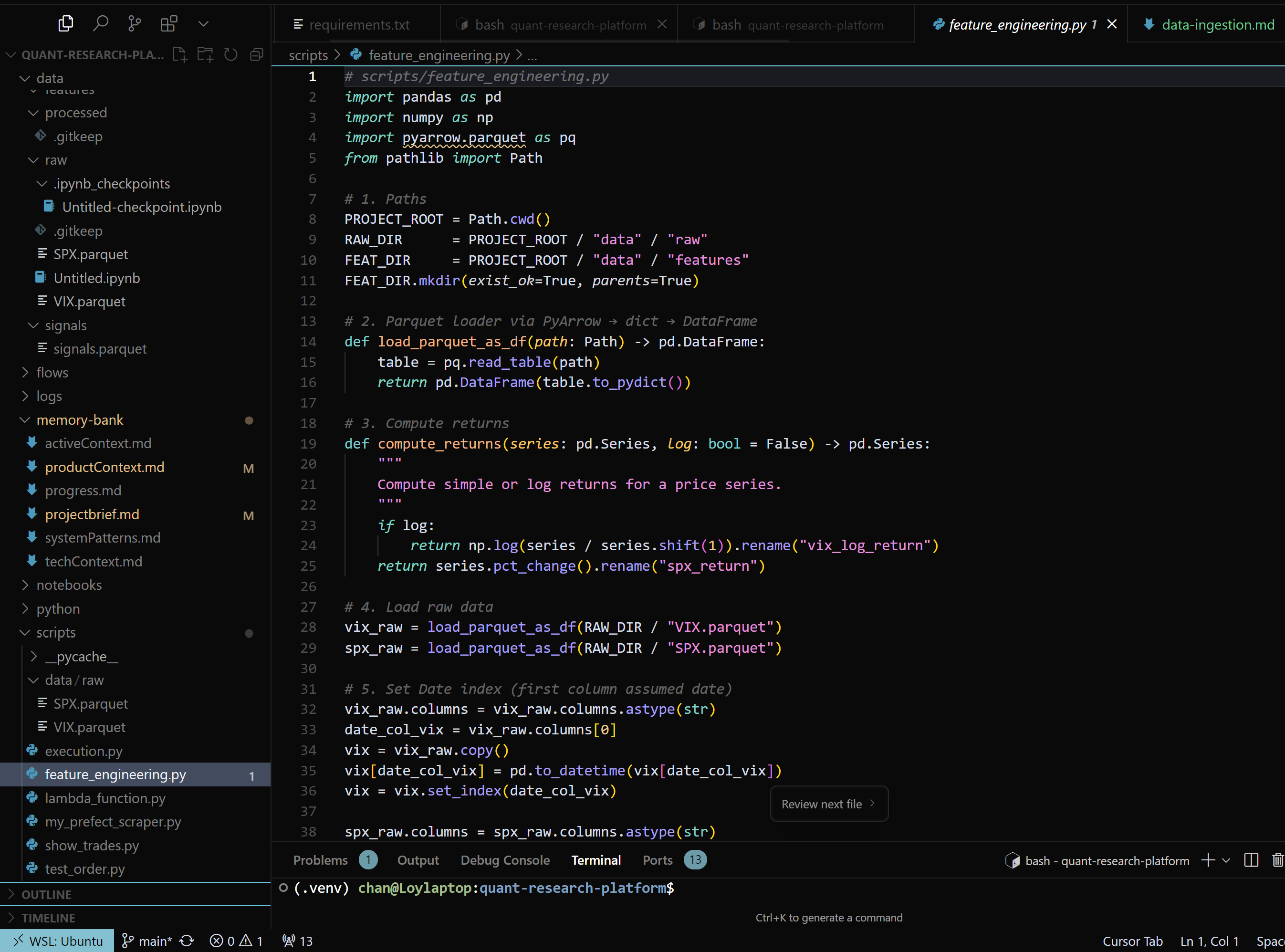

Introduction

I focused on building a reliable data ingestion layer that pulls market and sentiment data into a raw data lake. My goal was to automate fetching CSV and Parquet files daily, validate them, and store them for downstream processes.

Data Sources

- Market data:

- VIX (CBOE) via CSV download

- SPX (S&P 500) via Parquet feed

- Treasury yields (1mo, 2yr, 10yr) from FRED API

- Credit spreads computed from corporate bond and Treasury rates

- Sentiment feeds:

- News headlines scraped using NewsAPI

- Twitter sentiment via Tweepy (filtered by finance keywords)

Architecture

+--------------------+

| Data Ingestion |

| - Prefect Flow |

| - API / CSV fetch |

+--------------------+

|

v

+--------------------+

| Raw Data Lake |

| - S3 (Parquet) |

| - Local backups |

+--------------------+

Implementation Details

-

Prefect Flow:

- Defined a daily schedule:

with Flow("ingest", schedule=Schedule(clocks=[CronClock("0 4 * * *")])) as flow: fetch_vix() fetch_spx() fetch_yield_curve() fetch_credit_spreads() fetch_sentiment() - Each task downloads or queries data, then writes to a local staging folder.

- Defined a daily schedule:

-

CSV & Parquet Handling:

- For CSV (VIX, yields), I used Pandas to read, validate, and convert to Parquet:

df = pd.read_csv("vix.csv", parse_dates=["Date"]) df["VIX"] = df["Close"].astype(float) df.to_parquet("raw/vix.parquet", index=False) - For Parquet (SPX), I read directly and verified schema:

df_spx = pd.read_parquet("spx_feed.parquet") assert "Close" in df_spx.columns df_spx.to_parquet("raw/spx.parquet", index=False)

- For CSV (VIX, yields), I used Pandas to read, validate, and convert to Parquet:

-

FRED API for Yields:

- Used

fredapi:from fredapi import Fred fred = Fred(api_key="YOUR_KEY") tarex = fred.get_series("DGS10") df_yield = pd.DataFrame({"Date": tarex.index, "Yield10": tarex.values}) df_yield.to_parquet("raw/yield_10y.parquet", index=False)

- Used

-

Credit Spreads Calculation:

- Merged corporate bond yields (from CSV) with Treasury yields to compute spread:

df_corp = pd.read_csv("corp_bonds.csv") df_treas = pd.read_parquet("raw/yield_10y.parquet") df_merge = pd.merge(df_corp, df_treas, on="Date") df_merge["CreditSpread"] = df_merge["CorpYield"] - df_merge["Yield10"] df_merge.to_parquet("raw/credit_spreads.parquet", index=False)

- Merged corporate bond yields (from CSV) with Treasury yields to compute spread:

-

Sentiment Fetch:

- NewsAPI for headlines, stored JSON → DataFrame with sentiment score (using

textblob):from newsapi import NewsApiClient newsapi = NewsApiClient(api_key="KEY") articles = newsapi.get_everything(q="finance", from_param=today) df_news = pd.DataFrame(articles["articles"]) df_news["sentiment"] = df_news["description"].apply(lambda t: TextBlob(t).sentiment.polarity) df_news.to_parquet("raw/news_sentiment.parquet", index=False)

- NewsAPI for headlines, stored JSON → DataFrame with sentiment score (using

-

Storage in S3:

- After validation, each Parquet file is uploaded to an S3 bucket:

import boto3 s3 = boto3.client("s3") s3.upload_file("raw/vix.parquet", "my-bucket", "quant/raw/vix.parquet")

- After validation, each Parquet file is uploaded to an S3 bucket:

Challenges & Solutions

- Schema drift: feed providers occasionally change column names. I added assertions and fallback renaming logic in each task.

- Network retries: some downloads failed intermittently. I wrapped fetch calls in retries with exponential backoff.

Next Steps

- Add delta ingestion for incremental updates (only fetch newest rows).

- Integrate streaming Kafka for live tweet ingestion.

- Build monitoring dashboards (Alert on missing data).

# This pipeline laid the foundation. Next, I’ll build feature engineering on top of these clean raw tables.